The Homex story: A boom and a bust

Sam Zell was looking for opportunities, and he found a winner in Mexico.

The government was working with developers to build massive housing complexes for poor and working-class families outside every major city. With billions in government funds flowing into the housing market, builders stood to reap a bonanza.

Zell, a Chicago real estate billionaire, spotted a prospect in 2002 in the northern state of Sinaloa — a small construction company called Homex owned by four brothers of the De Nicolas family.

The brothers possessed the ambition. Zell, through his Equity International Investment Fund I, provided a boost of capital: $32 million.

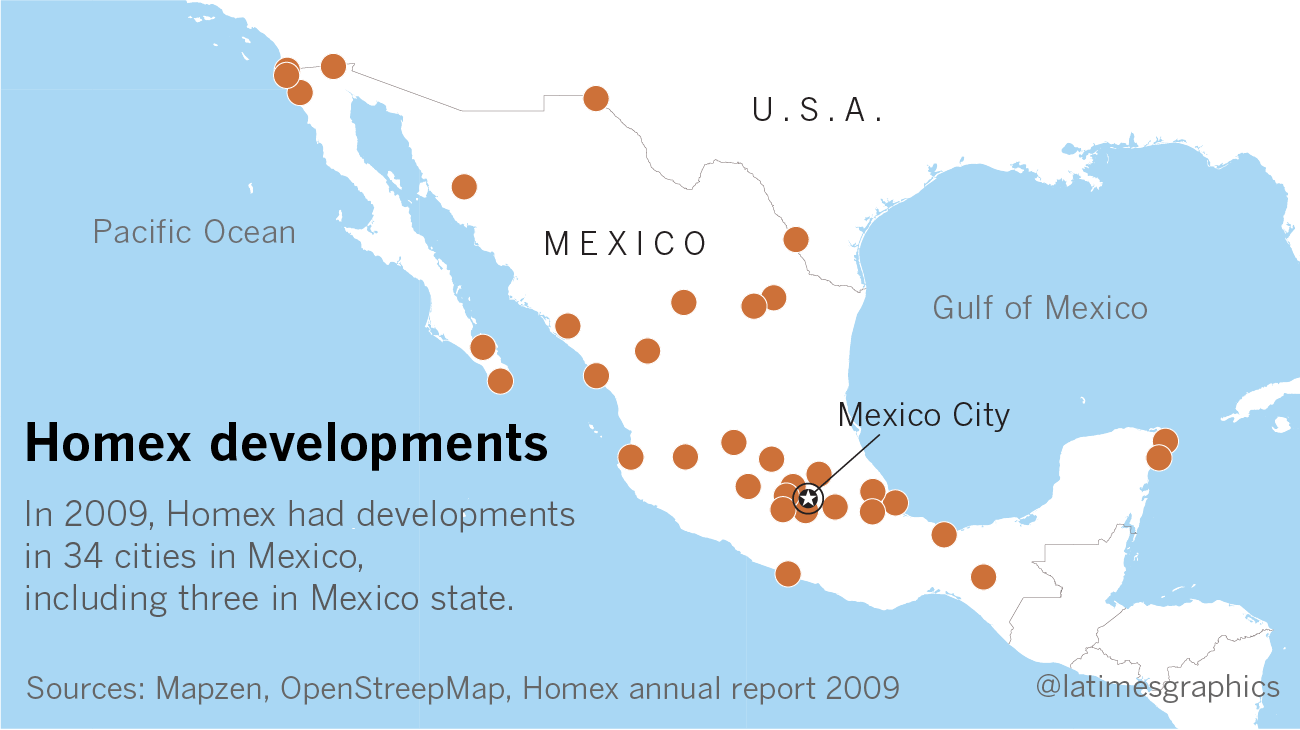

Over the next six years, Homex went from building 5,000 homes a year to building 57,000. It joined the ranks of North America’s largest home builders, broke ground on projects in Brazil and opened offices in Egypt and India.

The Homex story tugged at both the wallet and the heartstrings: Investors could earn big returns while helping solve global housing shortages. The World Bank, Wall Street investment banks, university endowments, foundations and U.S. pension funds invested billions in the company.

Homex’s valuation, $100 million when it went public in 2004, soared to $3 billion. Company executives went to the New York Stock Exchange to ring the closing bell, chanting “Homex! Homex! Homex!” The De Nicolas brothers traveled the world as ambassadors for Mexican entrepreneurship.

The big returns, however, masked the flaws that eventually gutted Mexico’s ambitious effort to house the masses. The developments were riddled with infrastructure and construction defects, and residents abandoned them by the thousands, helping trigger the collapse of the housing industry.

In 2014, six years after Zell’s fund sold off its shares, Homex fell into bankruptcy. This year, the U.S. Securities and Exchange Commission accused Homex of committing what is believed to be the largest fraud in Mexican history, saying it had reported “fake” sales of more than 100,000 homes. The allegations concerned activity that occurred after Zell’s fund divested, and Zell was not named in the complaint.

Today, with its broken-down, blighted and half-finished developments littering cities across Mexico, Homex is one of the country’s most despised companies. Dubbed “Robex” by some, the company is mocked on blogs and billboards, in punk rock songs and a Hitler-in-the-bunker internet spoof.

Long before it all came crashing down, there was one group that already knew how bad things were: the people who had to live in the houses Homex built.

Victor Ambrosio, a 27-year-old chicken vendor, and his parents bought a two-bedroom house in the Colinas de Santa Fe development, which opened in 2007 in Veracruz, on the Gulf of Mexico.

As the stock price soared, homeowners were suffering power outages and water shortages so acute that they once tried to flip over the sales office trailer where Homex employees had barricaded themselves.

“When I saw the model homes, I said ‘Wow,’’’ Ambrosio recalled. “But it was all smoke and mirrors. There were defects everywhere, like ticking time bombs.”

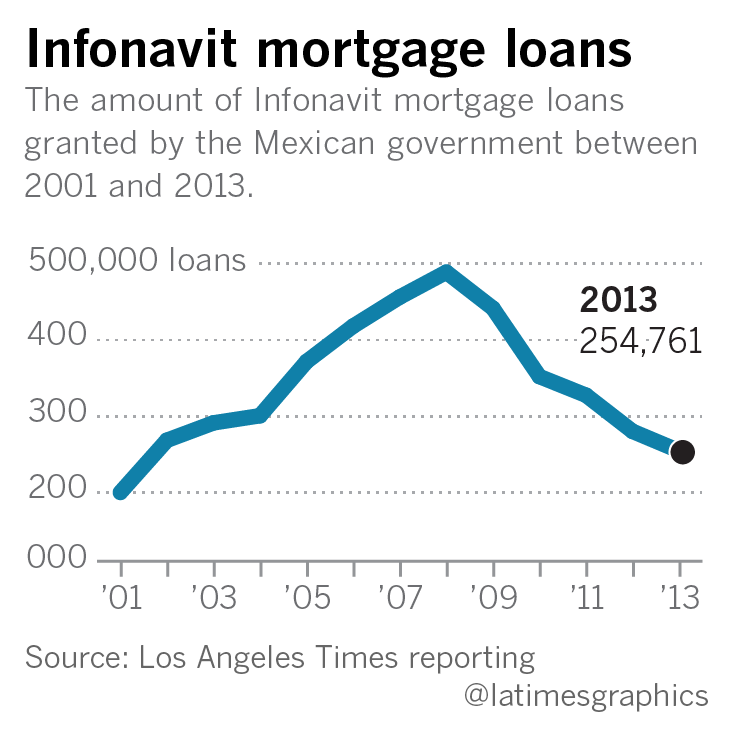

The company’s rise was powered by then-President Vicente Fox’s promise to succeed where his predecessors had failed in fulfilling the Mexican Constitution’s guarantee of “a dignified and decent” home for all citizens.

Fox unleashed Infonavit, Mexico’s giant housing-finance agency, which was flush with cash from employer contributions that workers could tap for home loans. Fox set lofty goals for the agency, pushing it to make hundreds of thousands of home loans every year.

Developers, guaranteed a pipeline of pre-qualified customers, would be able to sell homes as fast as they could build them.

Homex claimed to have perfected the mass production of affordable housing priced from $15,000 to $35,000. Executives boasted that construction crews could put up an entire house in one day.

It was an investor’s dream. Zell’s bets on U.S. properties — everything from office towers to trailer parks — had made him one of America’s wealthiest real estate magnates.

By 1999, Zell had turned his sights beyond the U.S., establishing Equity International Properties Ltd., a private equity firm focusing on real estate in emerging markets.

The company’s Equity International Investment Fund I concentrated on Mexico and aimed for a 20% annual rate of return for its U.S. investors, according to a fund profile by Preqin, a data company that tracks private equity funds. The investors included General Motors Investment Management Corp. and the John D. and Catherine T. MacArthur Foundation. The fund raised $368 million.

With $32 million of that money, Zell in 2002 purchased a stake in Homex worth about 26.5% of the company.

Equity International executives groomed the Mexican company for an initial public offering on the New York Stock Exchange. Homex adopted U.S. accounting standards, and its executives polished their English.

Equity International, which touts “proactive involvement in key business decisions” of its portfolio companies, expanded its role in Homex.

The fund’s chief executive, Gary Garrabrant, became Homex’s vice chairman. Zell traveled to Boston and New York to pitch Homex to investors, according to a 2005 story in the Wall Street Journal.

Homex’s housing starts jumped from 7,000 in 2002 to 13,000 a year later. Revenue tripled to $260 million. On June 29, 2004, Homex went public, raising $141 million.

The building spree went into overdrive. Already at work on projects in 16 cities, Homex broke ground on 17 more over the next few years.

In 2004, Fox attended a ceremony celebrating the construction of the 9,000th home at the Hacienda de Santa Fe development near Guadalajara.

Paul Wolfowitz, then president of the World Bank, lauded Homex in 2006 after company executives escorted him around the Real de San Jose development of 4,212 homes on the outskirts of Monterrey.

The bank invested more than $1 billion in Mexican housing, providing funds for the country’s development bank and taking equity stakes in mortgage lenders and construction companies, including Homex.

“I saw many compelling examples of the importance of the private sector’s role in offering opportunity for poor people to transform their lives and to give their children a better future,” Wolfowitz said in the bank’s annual report in 2006.

By 2009, an estimated 1 million people lived in Homex housing.

“We believe that a house is very, very important, and everybody needs a house,” then-Homex Chief Executive Gerardo De Nicolas said at an Anthony Robbins motivational seminar.

As the cheers for Homex reached a crescendo, Zell was pulling out. In 2006, he started selling off big chunks of the fund’s holdings, and by 2008 Equity International had divested the last of its Homex shares.

Equity International boasted publicly of its success in Mexico.

Profits from Homex topped $500 million for the fund’s investors, Garrabrant told Private Equity Real Estate Magazine in July 2009.

In 2010, two years after the fund divested from Homex, Zell wrote in a Mexican real estate magazine that he had brought U.S. standards of transparency to the Mexican company with his investment, “and we were paid for it.”

Zell and Garrabrant declined to comment. Zell makes no mention of Homex in his 2017 book, “Am I Being Too Subtle?,” an account of his investment strategies through the years. (Zell was chairman of Tribune Co. from 2007 to 2012, when it owned the Los Angeles Times.)

Cracks in Homex’s business model had been forming as early as 2004.

The company began work that year on the Las Almeras development in Ciudad Juarez, across the border from El Paso. It consisted of 1,303 homes in a dry lake bed — a site geologists had warned was prone to flooding.

A year later, Homex broke ground on the 4,000-home Costa Dorada development in a wetlands area of Acapulco — again failing to heed the warnings of geologists.

Both developments flooded repeatedly.

In 2007, Mexico’s Federal Consumer Protection Agency criticized Homex for construction failures at a Monterrey development called Barrio de la Industria.

The builder failed to properly grade the land, causing soil erosion and instability, according to an agency report that cited a study of the tract from the Autonomous University of Nuevo Leon. Walls cracked, concrete slab floors ruptured, sidewalks sank and rainwater puddled in patios and streets, the study found.

The agency also cited Homex for reneging on its promise of schools, underground utilities and high-quality materials at the development of 1,100 homes.

“The construction company deceived the consumers from the moment they bought the homes,” the report said.

The agency fined Homex about $500,000. The money was supposed to be used for repairs, but Cesar Salazar, the Monterrey development’s homeowner leader, said he didn’t see any were made.

Homex and the consumer agency declined to comment.

It was only the beginning of the unraveling. At Homex developments across Mexico, defects revealed themselves with the first rains or turn of a faucet. Water systems failed. Pumps malfunctioned. Sewage treatment plants broke down. Poorly graded streets washed away.

From the mid to late 2000s, homeowner protests and waves of complaints broke out in almost all the cities where Homex was operating.

But during quarterly earnings calls with Wall Street analysts, Homex executives did not mention the growing social unrest and downplayed the problems completing infrastructure.

In 2007, a Homex executive told analysts that the firm was scheduled to break ground on thousands of new homes at Santa Teresa, its giant development in Huehuetoca, north of Mexico City.

“We are upgrading the infrastructure to be able to deliver those homes in the beginning of next year,” said Alan Castellanos, Homex’s chief financial officer.

He didn’t mention the pervasive power outages in the parts of the development Homex had already built.

Every year, Homex filed disclosures with the SEC, and almost every year the agency raised questions about the firm’s accounting and reporting practices. It asked in 2006 why the company’s net income was reported differently under Mexican and U.S. accounting rules.

In 2008, the SEC asked for more information about the number of homes sold and unsold, and questioned the company’s practice of including inter-company loans as cash flow.

In 2011, the agency, after noting errors in Homex’s filings, questioned the effectiveness of the company’s disclosure procedures and ordered it not to make “unpermitted changes” on certification documents.

Homex representatives, in media reports, blamed problems on homeowners and local governments, saying their failure to maintain homes and streets contributed to the decay. The company was merely following local zoning laws that permitted development in high-risk zones, they said.

But housing experts and local officials said that Homex, boasting Wall Street credentials and a social mission backed by the Mexican president, was able to steamroll municipal regulators and local officials.

Even as the problems in Homex developments became evident, the company continued to receive fast-track approvals. Existing projects were shortchanged so the company could get to work on new ones, said Jose Becerra O’Leary, a former top official at the Veracruz regional office of Mexico’s federal electric utility.

Instead of completing infrastructure, Homex “just took the money for other things … and left behind problems,” Becerra said. “The problem lies in why authorities kept permitting this.”

Homeowners’ complaints about shabby construction and unfinished infrastructure had gotten little attention. Then Homex and the government confronted a more serious problem: Residents started packing up and moving out.

By the late 2000s, blocks of abandoned homes blighted developments across the country. Squatters and gangs moved in. Crime spiked, generating more departures.

A 2015 report by the Paris-based Organization for Economic Cooperation and Development estimated that as many as 500,000 homes built by Homex and other developers between 2006 and 2010 were vacant.

In response, Fox’s successor, President Felipe Calderon, began steering Infonavit loans away from the troubled suburban developments toward projects in big cities. The shift raised concern on Wall Street because urban developments called for high-rise buildings, which require more time and money to complete.

Homex executives reassured investors in a quarterly earnings call in May 2011, saying the company’s unique construction technology was adaptable to “vertical housing.”

“This is nothing new and does not present an obstacle for Homex,” said Gerardo de Nicolas, Homex’s chief executive officer.

In its 2011 annual filing with the SEC, Homex presented a picture of financial stability.

It reported selling 52,486 homes.

In fact, Homex sold 11,006 homes that year, the SEC said in March, asserting that the company had inflated revenue by counting sales of homes that were never built.

The SEC, unbeknownst to investors, had been investigating Homex since at least July 2012, when the company was made aware of the probe. That same year, Homex secured a $75-million credit line from the World Bank and raised $400 million on the U.S. bond market.

“Homex’s capable management team executes strong internal controls, construction expertise and efficient practices,” Moody’s Investors Service said in a 2012 report that gave the company’s bonds a “stable rating outlook.”

Shortly after President Enrique Peña Nieto took office in late 2012, Homex’s troubles mounted. He announced that almost all future government housing loans would be for urban high-rises.

“Working together we can build dignified cities, houses with sufficient space and with basic infrastructure that elevates the quality of life of all Mexicans,” Peña Nieto said, in a swipe at the policies of his predecessors.

The shift was devastating for Homex.

Revenue dropped 46% in the first quarter of 2013, and 84% the next.

Quarterly earnings calls turned tense as some analysts accused Homex of misleading investors with overly optimistic profit estimates.

“Why would we believe you now after three years of just completely failing to come even remotely close to your guidance?” said Denis Parisien, an analyst with Deutsche Bank during a conference call in February, 2013. “I speak to a lot of investors, so this is … the frustration that I’m hearing.”

Desperate, Homex turned to Zell in April 2014, asking its former partner for a $135-million credit line from his Credit Opportunities Fund.

There’s no evidence that Homex received the credit line.

Homex’s stock price, which had peaked at $69 in 2008, fell to $1 per share.

In July 2014, the company filed one of the largest corporate debt restructurings in Mexican history. It listed $8 million in cash and $2.5 billion in debt.

Executives slashed payroll, cut off suppliers and suspended payments to utility companies.

Like a rolling blackout, lights went out in one Homex development after another across Mexico.

Chaos descended on Culiacan, capital of the northern state of Sinaloa and the company’s hometown.

Outside Homex’s corporate offices on Boulevard Alfonso Zaragoza Maytorena, hundreds of fired employees protested over unpaid wages.

Across town in bankruptcy court, global investors who had purchased bonds from Homex and extended credit lines totaling more than $1 billion demanded payment.

They included Pacific Investment Management Co., the Newport Beach bond company commonly known as Pimco, which loaned Homex and other Mexican home builders tens of millions of dollars; the World Bank, which poured more than $1 billion into the Mexican housing sector; and Bank of America; according to bankruptcy documents filed by Homex in Mexican federal court.

The former bondholders and creditors agreed to forgive their debt in exchange for equity in the firm. They would own from 75% to 90% of the company’s shares under the restructuring agreement.

It is unclear which of Homex’s former bondholders remain as shareholders in the restructured company. Some of the original creditors sold their bonds at discounted prices to U.S. hedge funds that specialize in distressed-debt opportunities.

Among the hedge funds represented on the company’s bankruptcy restructuring committee were Alden Global Capital, River Birch Capital, BSOF Master Fund, which is managed by Blackstone Inc., and BlueCrest Capital, once the world’s largest hedge fund.

None of the firms would comment for this article.

In late 2015, Homex emerged from bankruptcy with what it said was a new approach “designed to meet its obligations and generate value to its stakeholders.” The new Homex would build upscale homes for middle-class buyers.

In March of this year, the company was jolted by U.S. regulators, who slapped the company with a securities fraud complaint. The evidence came from high above.

The SEC, announcing the conclusion of its investigation, released a satellite image of a Homex development in the central state of Guanajuato.

The Benevento development was billed as one of the company’s top-grossing projects. Homex said in its annual SEC filings that hundreds of units had been sold there in 2010 and 2011.

But the satellite image, taken in 2012, showed an empty patch of dirt streets.

The SEC said the ruse was part of a “massive fraud” by Homex to inflate revenue by $3.3 billion from 2010 to 2012. Top executives, including longtime CEO De Nicolas, kept two sets of financial records, according to the SEC complaint, and reported bogus revenue while Homex was listed on the New York Stock Exchange and raising $400 million from investors.

“Homex systematically and fraudulently reported revenue from the sale of tens of thousands of homes annually that it had neither built nor sold,” the complaint said.

The SEC said Homex had also defrauded Mexican banks in a $7.7-billion Ponzi-like check-kiting scheme.

Without admitting or denying wrongdoing, Homex settled the case in March with the SEC, agreeing to a five-year ban from U.S. stock markets. Mexico’s National Banking and Securities Commission fined the company $1.2 million.

It’s far from clear whether anyone will be held accountable.

The SEC, in a separate action in October, filed securities fraud charges against De Nicolas and three other former Homex executives who had already resigned from their posts. The agency is seeking unspecified civil penalties and the return of any ill-gotten gains.

But it’s uncertain whether any of the defendants will appear to address the charges in federal court in San Diego.

In a statement Thursday, Homex said it “has strengthened internal control mechanisms to improve its corporate governance practices,” but did not comment directly on the SEC actions.

The company did not respond to requests for comment from the executives.

They are believed to be still living In Mexico, where federal authorities have declined to comment on whether they have launched an investigation.

Homex is now on the comeback trail.

In October, Homex received $48 million in new capital from investors and is aiming to sell 1,800 homes this year.

“The housing industry in Mexico continues to be a key sector in the economy and development of the country due to the necessity of new housing,” Jose Baños Lopez, the company’s new general director, said in a news release.

The company promised to make repairs to existing developments, but there are few signs of fixes, even in tracts where people line up for water at spigots or flee their homes after they collapse in ruins.

In August, two four-story condominium buildings in separate Homex developments toppled during a tropical storm in the Cabo San Lucas area. Residents and civil engineering groups had complained for years that the structures, which were constructed in creek beds, were not safe.

The wreckage has turned into hazard-filled playgrounds picked through by children and looters.

Meanwhile, at the Parque San Mateo development 30 miles north of Mexico City, Homex salespeople keep pitching dreams of homeownership. A wide avenue lined with fluttering banners leads to the sales office, which features a large mural of a smiling family enjoying a picnic.

But water shortages are a consistent problem, residents say, and rumbling diesel generators supply power to hundreds of residents — a noisy workaround for an unfinished electrical system.

Many residents have lived in the half-finished development for years but don’t have deeds to their homes. Homex never paid the escrow officer to complete the transactions, they say.

Yet sales agents greet potential buyers every day, handing them a brochure that says the homes, priced at $20,000 each, will increase in value as much as 40%.

“Your dreams,” the brochure reads, “are about to be transformed.”

Times researcher Cecilia Sanchez in Mexico City contributed to this report.

Credits: Produced by Andrea Roberson, graphic by Swetha Kannan