CRE in Southern California is under significant pressure from macro economic volatility

- Share via

Jump to data:

- Los Angeles County (LA Office Market / LA Industrial Market)

- Orange County (OC Office Market / OC Industrial Market)

- Inland Empire (IE Office Market / IE Industrial Market)

- San Diego County (SD Office Market / SD Industrial Market)

Tariffs, high interest rates and elevated construction costs in the wake of the tragic wildfires any of these could profoundly impact the Southern California real estate market. However, the trio of factors combined has left many involved in the industry facing unprecedented challenges.

Other factors such as federal leasing, which has long been one of the major pillars of office leasing activity in Southern California, could be impacted by federal government cost-cutting measures that could put existing leases under review and slow expansion or new deals. That compounds factors for office landlords who have struggled with office occupancy as companies re-evaluate workplace strategies. In areas such as Downtown Los Angeles, the office vacancy rate was above 31%, according to the most recent data from Cushman & Wakefield.

In the industrial sector, a surge of imports was observed at the ports as retailers raced to bring goods into the U.S. ahead of new tariffs. Activity was supported by labor strikes at Eastern and Gulf Coast ports that temporarily prompted shippers to divert some cargo to the West Coast, subsequent to a deal that was ratified in February.

Those factors, however, have been overshadowed by the prospect of a trade war, which has the potential to be the single-greatest factor that will impact the economy moving forward. The policies set by the federal government roiled capital markets and directly impacted the commercial real estate sector.

The uncertainty surrounding policies led to firms such as Calabasas-based Marcus & Millichap to host a call with experts to discuss potential outcomes for real estate investors, brokers and other interested parties.

“We felt that there’s a need for an update and clarity,” said Hessam Nadji, chief executive and president of Marcus & Millichap Inc., on the real estate investor update call. “We want to compare notes on what we see in the marketplace at a time when a lot of variables are conflicting.”

Nadji spoke about the recent impact of macro policy changes with Mark Zandi, chief executive of Moody’s Analytics, and Jeffrey D. DeBoer, chief executive and president of the Real Estate Roundtable. Zandi stressed that uncertainty around economic policy, particularly around the global trade war, is doing damage to consumer sentiment.

He stated that without a shift in policy with regard to the trade war, risks are high that the country suffers an economic downturn even though the economy fundamentally began 2025 in a good place.

LOS ANGELES COUNTY

The Los Angeles office market reported its 11th consecutive quarter of negative net absorption, and the vacancy rate climbed to 24.5% as the office market faces headwinds from low tenant demand and re-evaluation by many companies of their long-term space needs, according to data from Cushman & Wakefield. Market-wide asking rents remained relatively stable at $3.60 per square foot per month on a full-service gross basis. Rates are highest in West Los Angeles, where the overall asking rate was $5.14 per square foot per month. The legal sector remained a leading source of leasing activity, accounting for over 383,000 square feet in new leases and renewals, including Loeb & Loeb’s 139,200-square-foot lease in Century City.

In industrial, vacancy has climbed to 4.9%, the highest in a decade following the 10th straight quarter of occupancy losses. Losses have been spread throughout the county with all six submarkets surpassing 3.0% and three areas above 5.5% vacancy. The availability rate, which includes marketed but not vacated, reached 6.5%, which suggests additional occupancy losses. Industrial rents spiked during the pandemic but have since fallen for six straight quarters in L.A. County. Nevertheless, those rates are still more than 50% higher, on average, compared with 2019. Industrial asking rates are projected to improve in 2026.

LA County Office Market

LA County Industrial Market

ORANGE COUNTY

The overall office vacancy rate in Orange County increased to 19.2% in Q1 2025 and has increased from about 10% over the past five years as the office market has dramatically changed. Bright spots for the office market include life science and healthcare, with leases from Tarsus Pharmaceuticals and St. Joseph Health System in the Irvine Spectrum submarket. The average asking rents for all property classes have remained stable over the past year as landlords enhance concession offerings, such as longer free rent periods and higher tenant improvement allowances. Newly developed Class A properties with top-tier amenities can reach $5.95 per square foot per month.

On the industrial side, the vacancy rate ticked upward for the ninth consecutive quarter to 4.2% as net absorption was negative for the sixth consecutive quarter. The losses were widespread with declines in each of the four subregions. The rise in overall vacancy was largely driven by tenant departures and speculative developments that were completed with tenant commitments. There is more than 500,000 square feet of new construction vacant.

Landlords have strong competition and may increase concessions, flexibility or offer discounted rent. An additional 2.7 million square feet were under construction, with some pre-leased. Orange County industrial sales activity surged to $573 million, up 49% compared with the year prior as investors showed a renewed interest in the market.

OC Office Market

OC Industrial Market

INLAND EMPIRE

The Inland Empire commercial real estate market is dominated by industrial warehouses that service the ports of Los Angeles and Long Beach. The overall vacancy rate dropped to 7.4%, the first decline since early 2022. The drop was attributed to 3.2 million square feet of net absorption, although factors indicate that long-term challenges persist. The availability rate rose due to excess supply that includes sublease listings. Sublease space accounted for 22.4% of available inventory, which rose to 10.5% as tenants consolidated footprints and made excess space available.

Sublease vacancies placed downward pressure on asking rents. Sublease asking rents were $0.87 per square foot per month on a triple net basis, far lower than the $1.23 per square foot direct asking rate. The weighted average of all proper- ties put the overall asking rate at $1.18 per square foot, a decline of 10.8% year over year. Declines in asking rates are projected to moderate by year-end as the pipeline for new construction, which has been robust for more than a decade, fell to its lowest level since 2014 with 11 million square feet underway. The Inland Empire office market has the lowest vacancy rate among major Southern California markets at 8.9%, which is down slightly year over year. The market offers an affordable option over coastal cities and is attractive to health care providers and local businesses. Average asking rates declined to $2.23 per square foot per month on a full-service gross basis, which was a 0.4% decrease.

IE Office Market

IE Industrial Market

SAN DIEGO

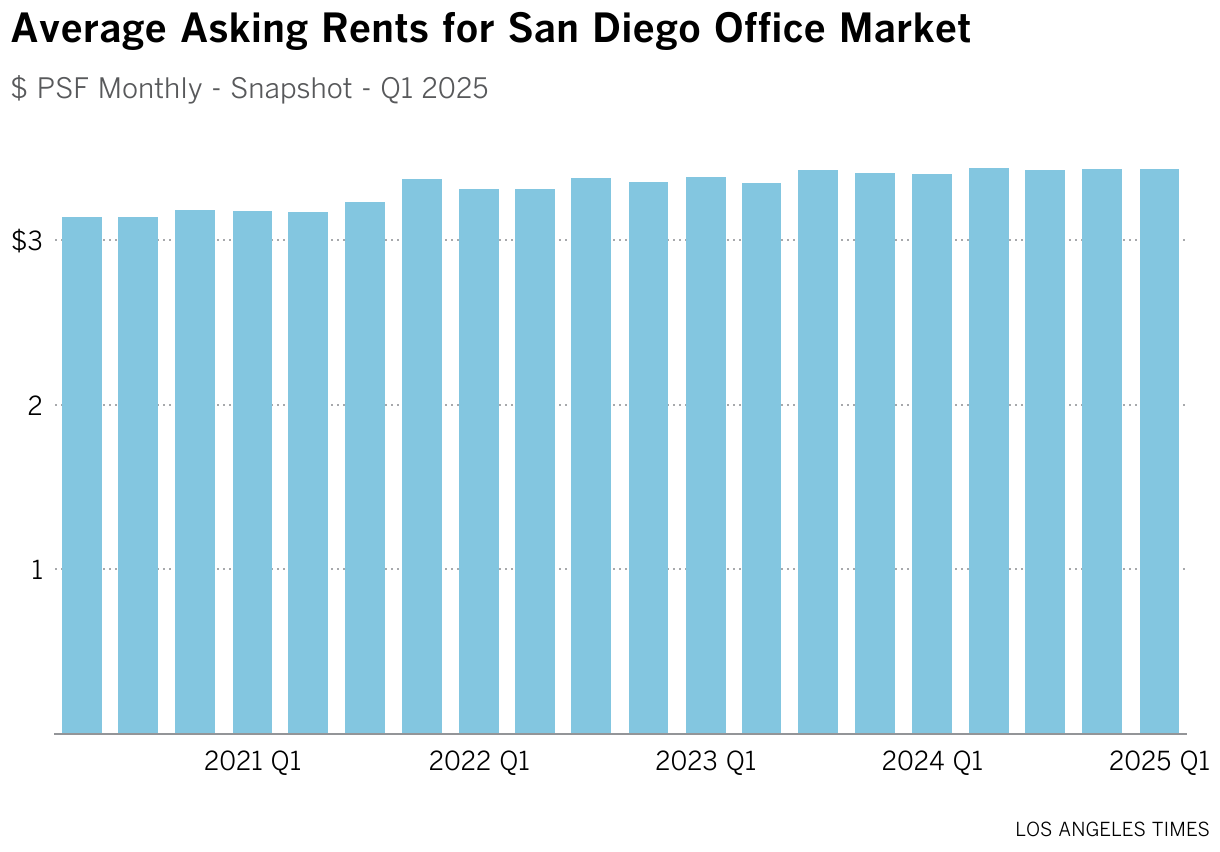

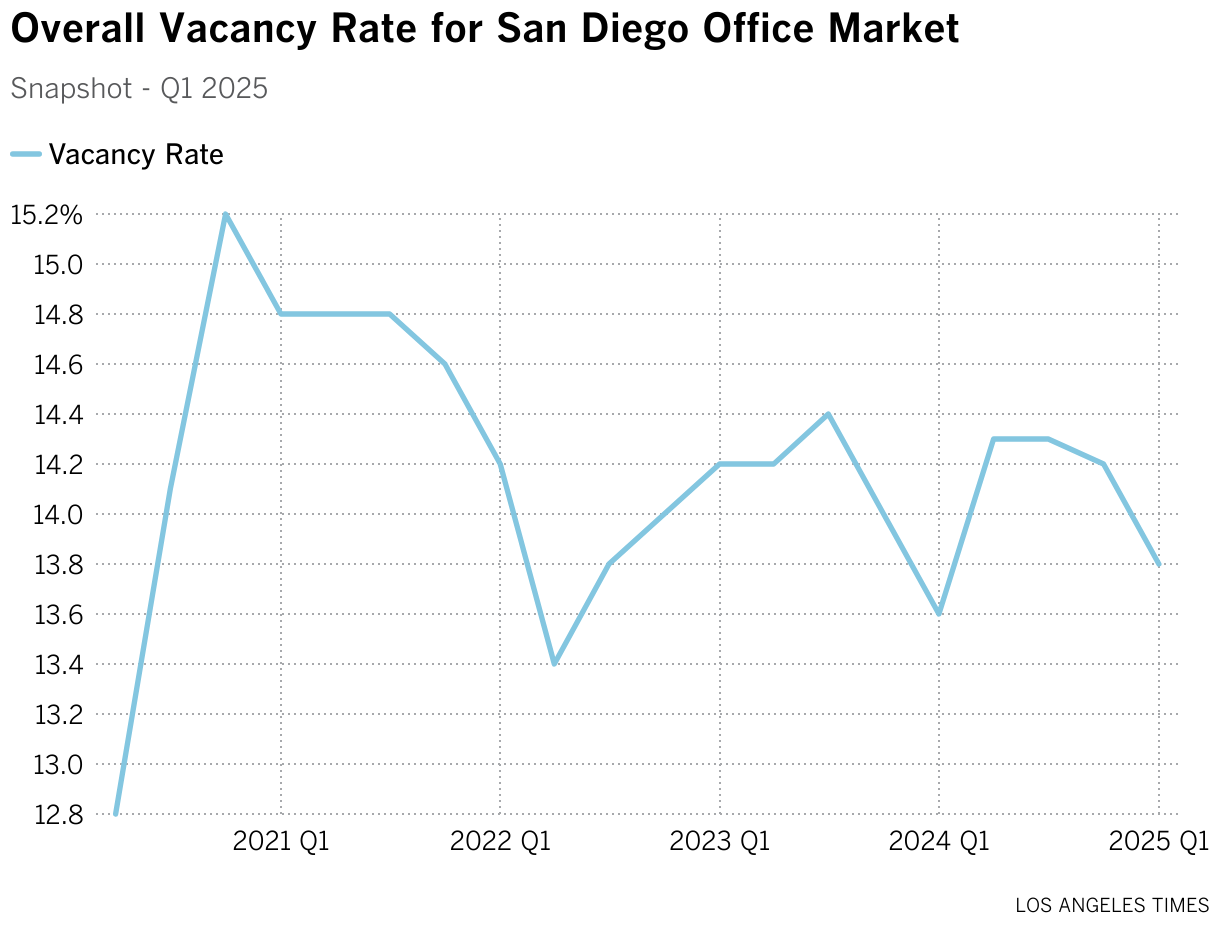

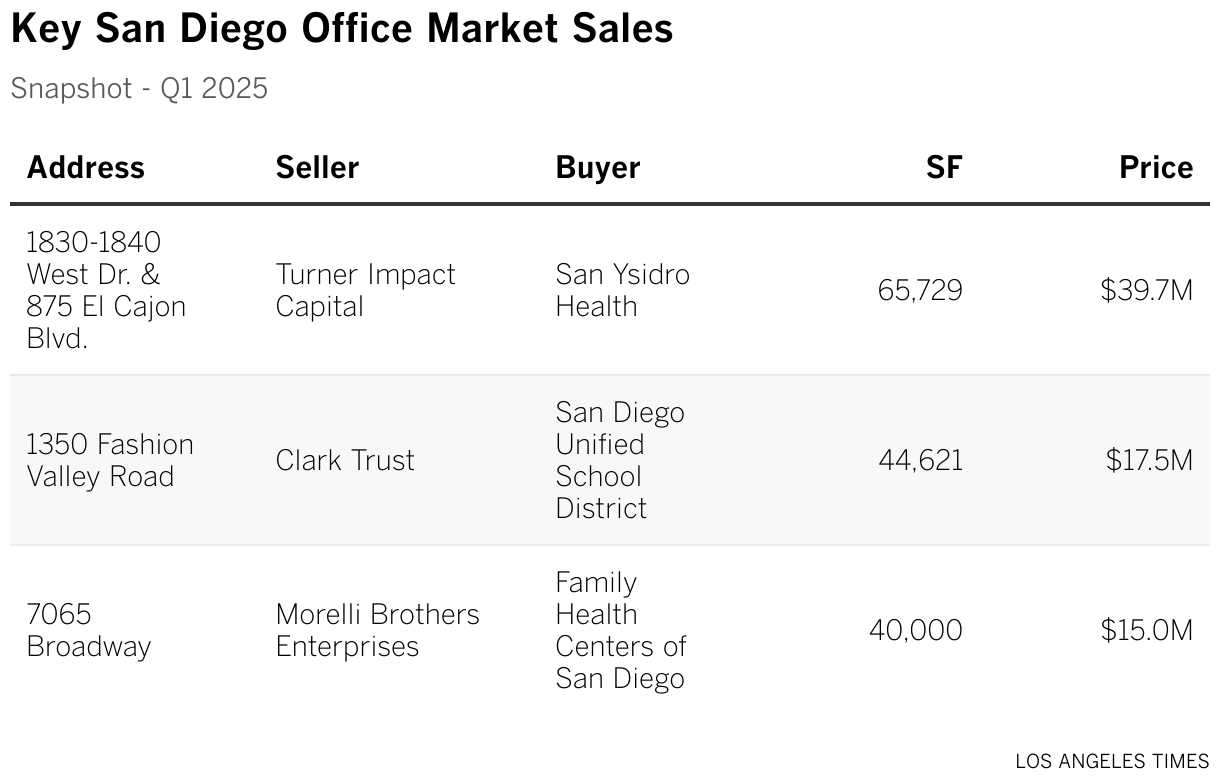

San Diego’s office vacancy rate was 13.8%, which was slightly higher than the prior year. The market had positive net absorption of 331,634 square feet, according to data from Cushman & Wakefield driven by Class A properties. ClassBand C buildings, which typically have fewer amenities and are located in less desirable areas, had negative net absorption of 149,000 square feet. Direct vacancy in many suburban submarkets has not risen enough to trigger price drops; the average asking rate was $3.44 per square foot per month.

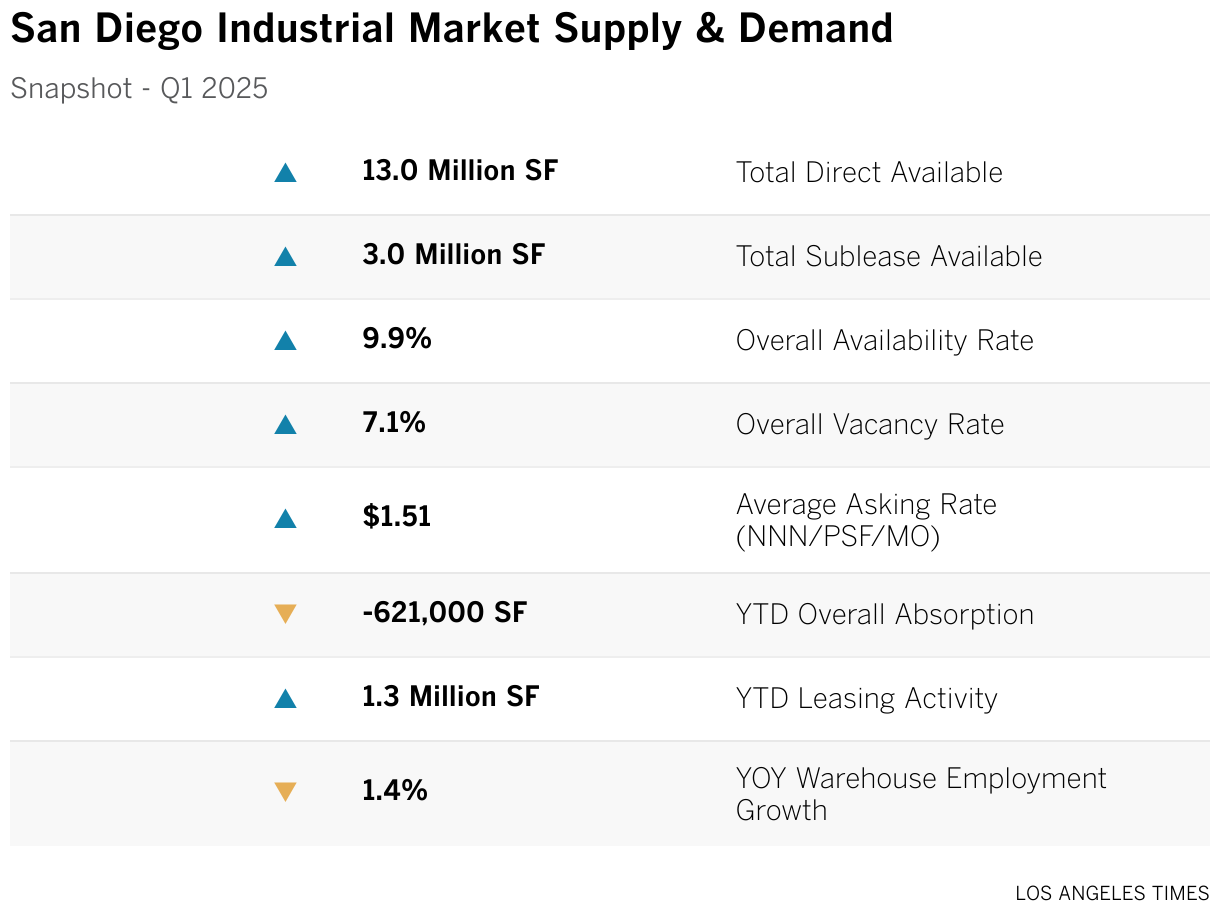

San Diego’s industrial vacancy increased to 7.1% despite several large tenants, such as Master’s Touch Brand, Land-Ron and Trident Maritime Systems occupying space. The county suffered its ninth consecutive quarter of occupancy losses. New leasing activity was up 29.8% quarter over quarter and 14.4% year over year.

The largest sector was manufacturing at 22%, followed by transportation, warehousing and utilities. Otay Mesa had the largest share of leasing at 31%.

The average asking rate held steady year over year at $1.51 per square foot per month on a triple net basis. There is more than 4 million square feet of demand from new tenants projected over the next two years. Manufacturing is a key driver, but the area’s economy includes defense, technology and life sciences.

SD Office Market

SD Industrial Market

More Stories